How Much Credit Card Debt Is Too Much? Run the Snapshot

The total balance is the number that scares you. These four numbers are the ones that tell you what is really going on.

Almost every conversation about credit card debt starts with the wrong number. Someone says “I have $8,000 in credit card debt” and the room nods solemnly, like that single figure tells you everything you need to know. It does not. The total balance is the headline. The story is in four other numbers that almost nobody knows off the top of their head.

If you want to know whether your credit card debt is manageable, getting dangerous, or already past the point where you should be calling for help, you have to run a snapshot. Not a payoff plan. Not a budget. Just a clear eyed look at where you stand on this exact day.

Here are the four numbers that matter, what each one means, and where the line is between fine and not fine.

Number One: Total Balance

Start by adding up every credit card balance you carry. Not the cards you pay off every month. Just the ones with a balance that rolls over to the next statement. Be honest. If there are six cards, list six cards. If there is one card you have been quietly ignoring because the balance keeps creeping up, that one goes on the list too.

The total balance by itself does not tell you whether you are in trouble. A $15,000 balance on a household income of $250,000 is annoying but survivable. A $5,000 balance on a household income of $35,000 is a five alarm fire. Context matters more than the raw number. But you cannot have the conversation at all without the total in front of you.

One useful rule of thumb: if your total credit card balance is more than 20% of your annual take home pay, you are in a zone where the math gets ugly fast. Below that, you can usually pay your way out. Above it, the interest starts compounding faster than most people can keep up with.

Number Two: Weighted Average APR

This is the number nobody talks about. Your weighted average APR is the true cost of your debt, accounting for which cards hold most of the balance. If you have $9,000 sitting on a 26% card and $1,000 on a 14% card, your weighted APR is about 25%, not the simple average of 20%. That eleven point difference matters when interest compounds daily.

Most people in serious credit card debt have a weighted APR somewhere between 22% and 28%. According to data from the Federal Reserve Bank of St. Louis, the average APR on credit cards accruing interest sat above 22% throughout 2025, the highest level on record since the series began in 1994.

If your weighted APR is above 24%, you should pick up the phone and call your highest rate card today. Ask for a reduction. Tell them you are a long time customer with on time payments and you are shopping for balance transfer offers. Many issuers will drop your rate two to five points just for asking. That single phone call can save you hundreds of dollars a year and it takes about ten minutes.

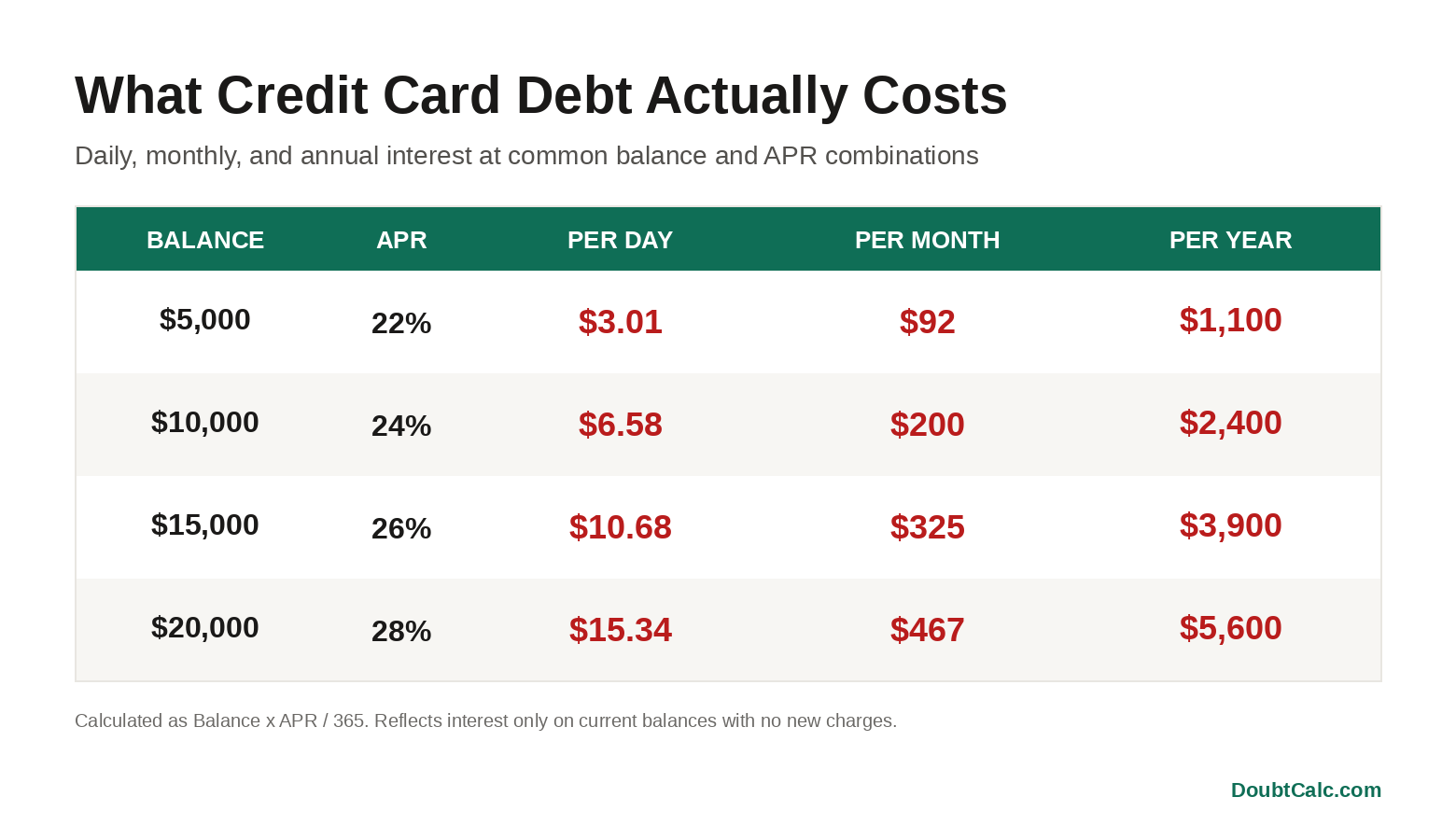

Number Three: Daily Interest Burn

This is the number that wakes people up. Your daily interest burn is what your current balances generate in interest every 24 hours, before you make a single new charge. It is the amount of money your debt costs you while you sleep, while you eat lunch, while you sit in traffic.

The math is simple. Take each card's balance, multiply by its APR, divide by 365. That is what that card costs you per day. Add them up across every card and you have your total daily burn.

A $10,000 balance at 24% APR burns about $6.58 per day. That is $46 a week. That is $197 a month. That is $2,400 a year going to interest alone, never touching the principal. And that is just one card. If you carry $20,000 spread across three cards at 22% to 28%, your daily burn is closer to $13 or $14 a day. Five thousand dollars a year that you will never see again.

Run those numbers for your own debt right now using the Credit Card Debt Calculator and write the daily burn number on a sticky note. Put it on your wallet. Every time you reach for a card, you will see what you are paying for the privilege of carrying the balance.

Number Four: The 12 Month Trajectory

The last number is the one that tells you which direction you are headed. If you keep paying only the minimum payment on each card, add no new charges, and your APR stays the same, what will your total balance be 12 months from today? Higher than today? Lower? About the same?

This is the trajectory test. If your projected balance one year from now is lower than today's, your minimums are at least covering interest plus a little principal. You are moving in the right direction, even if slowly. If the projected balance is the same as today, you are running in place. Every dollar of every minimum payment is going to interest. If the projected balance is higher than today, your minimums are not even covering the interest. The debt is growing while you are paying it. That is the financial version of bailing water out of a boat with a hole in it.

Roughly one in five Americans with credit card debt is in that third bucket according to recent Bankrate surveys. Minimum payments cover interest plus one or two percent of principal, and as the balance climbs, the minimum climbs with it, and the household ends up paying more every month while the total owed never goes down.

The Three Zones

Once you have those four numbers in front of you, you are in one of three zones.

Green zone: manageable. Your total balance is under 20% of your annual take home pay, your weighted APR is under 22%, your daily burn is small enough that doubling your minimum payments would pay you off in three years or less, and your 12 month projection shows a meaningful decline. You are uncomfortable but not in danger. Make a payoff plan and stick to it.

Yellow zone: getting dangerous. Your total balance is 20% to 40% of annual take home, your weighted APR is 22% to 26%, your daily burn is hundreds of dollars a month, and your 12 month projection shows only a small decline or running in place. This is the zone where most people are. The math still works in your favor, but only if you act aggressively. Call your cards and ask for rate reductions. Look at a balance transfer card with a 0% intro period. Pick a payoff strategy and start cutting somewhere in your budget to feed extra payments to your highest rate card.

Red zone: out of control. Your total balance is more than 40% of annual take home, your weighted APR is above 26%, your daily burn is enough to fund a real expense like a car payment, and your 12 month projection shows the balance growing. The math is working against you and the gap widens every month. At this point, do not try to solve it alone. The National Foundation for Credit Counseling provides nonprofit credit counseling at no cost or very low cost. They can negotiate with your card issuers on your behalf and set up a debt management plan that often cuts interest rates in half. This is the move. It is not a failure. It is a legitimate, well established tool for getting out of a hole that is too deep to climb out of yourself.

What to Do With Your Snapshot

The point of a snapshot is not to feel bad about it. The point is to know exactly where you stand so the next move is obvious. Most people never run these numbers because they are afraid of what they will see. That fear is the most expensive feeling in personal finance. Avoiding the numbers is what lets the daily burn quietly drain thousands of dollars a year out of your accounts while you pretend it is not happening.

Once you have the four numbers, the next step depends on which zone you are in. Green zone: run the Debt Payoff Calculator to compare snowball and avalanche strategies and pick the one that fits your personality. Yellow zone: do the same thing, then call your highest rate card and ask for a reduction or look into a balance transfer offer with a long 0% intro period. Red zone: call a nonprofit credit counselor before another month of interest hits.

Whatever zone you are in, you are better off knowing than guessing. Run the Credit Card Debt Calculator and let the four numbers tell you the truth. It takes about three minutes. The number you see at the end of those three minutes is the one that finally makes the situation real enough to act on.

This article is for informational and educational purposes only and does not constitute financial, legal, or tax advice. APR ranges, average debt figures, and minimum payment formulas vary by issuer and change over time. If you are struggling with debt, consider speaking with a nonprofit credit counselor or a licensed financial professional.